Stockpickers often talk about finding companies with high barriers to entry – or a defensive moat – that prevents competitors from muscling into their territory. The same theory can be applied to selecting funds and managers.

Kier Boley, chief investment officer of alternative investment solutions at Union Bancaire Privée (UBP), said that a manager’s unique alpha – the way they outperform – can be compared to a radioactive substance because it has a half-life and it decays.

In other words, if an investment strategy works, other fund managers copy it, academic papers get written about it, competitors poach key staff and the advantage gets competed away.

UBP, which appoints third-party alternative investment managers to sub-advise its UCITS funds, partners with managers whose strategies and skills have a defensive moat, protecting them from decay.

One type of moat is a large team of specialist analysts who provide value-adding insights. For example, Brigade Capital Management, which sub-advises a credit long/short fund for UBP, has fundamental credit analysts on the ground in Europe and the US, Boley said.

Brigade’s moat also consists of its extensive experience investing across the credit spectrum spanning high yield, distressed debt and event-driven strategies. Because it has expertise in both stressed and distressed workouts, if an issuer gets into difficulties, Brigade does not have to sell it.

In the traditional equity space, Brown Advisory has gone the extra mile and amassed a team of investigative researchers who find out information to which its analysts don’t have access. For instance, before Brown Advisory invests in a healthcare stock, the researchers might go to a medical conference to ask doctors why they recommend a certain treatment.

Darius McDermott, managing director of Chelsea Financial Services, said that Allianz Global Investors also has a “grassroots team” who conduct non-traditional financial analysis. "Another example would be GQG who also hire non-traditional analysts, often former investigative journalists, who work alongside the investment managers," he added.

A complex, hard-to-replicate investment strategy provides another type of moat. The Campbell Absolute Return UCITS fund has four sub-strategies, a combination that is unique in the UCITS space and difficult for competitors to copy, Boley said.

First, Campbell & Co. looks at price patterns and short-term trends that span 10 days or fewer; the second strategy involves pattern recognition for trends lasting more than 20 days. The combination of the two trend-following strategies tends to smooth out returns.

Then there is a systematic macro strategy looking at the yield curve, rates and other economic data. And finally, Campbell’s fourth strategy predicts price moves in single stocks. Campbell aims to deliver 10% returns per annum with 10% volatility, so a Sharpe ratio of one.

A third type of moat is technology or trading infrastructure that would be expensive or difficult to replicate. Taking an example from the long-only equity world, Evenlode Investment Management has built its own in-house, forward-looking valuation model.

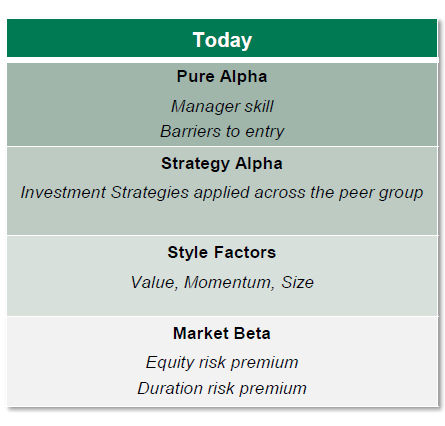

When researching an alternative investment strategy, UBP decomposes the performance to ascertain how much of the returns can be attributed to market beta (i.e. equity and bond market movements and the equity risk premium), or to style factors (such as growth, value or momentum), and then to strategy alpha (models and investment strategies that provide added value).

Finally, the icing on the cake is pure alpha – the fund manager’s skills and their ‘secret sauce’, which ideally would be protected by high barriers to entry.

Decomposing an alternative investment manager’s return streams

Source: UBP

After identifying how a manager delivers excess returns, UBP investigates whether those returns are likely to continue and what barriers to entry can protect the manager’s investment edge from being competed away. The chart below explores different types of defensive moat.

Pure alpha is protected by barriers to entry

Source: UBP

UBP’s alternative UCITS platform also includes an equity arbitrage strategy in partnership with Cheyne Capital and an environmental, social and governance (ESG) strategy managed by Bain Capital Public Equity, which applies a private markets approach to public markets.